>> Continued From the Previous Page <<

The IRS argued, and the court agreed, that these insurance proceeds should boost the company’s valuation as they represent a financial capability at the time of the shareholder’s death. The executor of Michael’s estate, Thomas Connelly, had valued the deceased’s shares at $3 million. However, an IRS audit and subsequent revaluation pegged the shares at over $5 million, considering the insurance payout, leading to a dispute over an additional $890,000 in estate taxes.

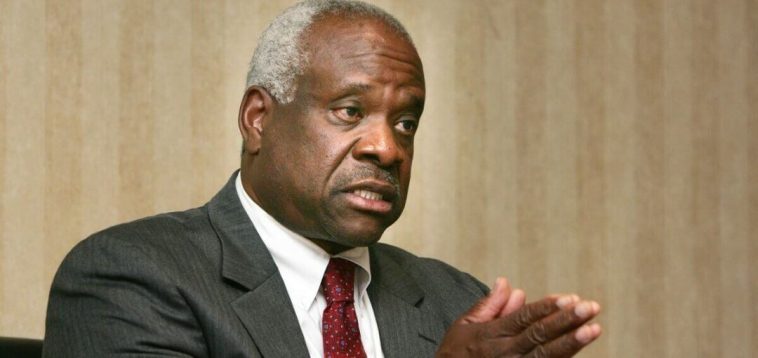

The justices’ decision centered on the financial dynamics within such corporate arrangements. “The central question is whether the corporation’s obligation to redeem Michael’s shares was a liability that decreased the value of those shares,” Justice Thomas wrote. “We conclude that it was not and therefore affirm [the decision of the Eighth Circuit].”

This ruling emphasizes that the obligation to buy back shares at fair market value should not be viewed as diminishing the worth of the shares or the corporation overall. This perspective could reshape how companies with similar buy-back agreements manage their financial strategies and estate planning.

Moreover, the decision highlights the nuances of valuing assets that are not publicly traded. “In many cases, fair market value can be determined through a straightforward analysis of public markets. But when a particular type of asset is not freely traded, fair market value must be determined on the basis of assessment and evaluation,” stated the petition.

Get Your FREE Trump 2024 Election Shirt – We’re Shipping It Right to You!

This ruling aligns with broader federal estate tax principles, where the value of the estate is calculated based on its status at the time of the owner’s death. This includes all assets and capabilities, such as life insurance that can be tapped for fulfilling corporate buy-back agreements.

This Supreme Court decision thus sets a clear guideline for estates involving closely held corporations, ensuring that life insurance proceeds used in such contexts are considered part of the fair market value of the deceased’s shares. This could have significant implications for estate planning and tax strategy for small to medium-sized family businesses across the nation.